BoC raises key rate to 1%, warns of further hikes to come Bank moves aggressively to wrestle inflation down from a 30-year high

Read this article for free:

or

Already have an account? Log in here »

To continue reading, please subscribe:

Monthly Digital Subscription

$0 for the first 4 weeks*

- Enjoy unlimited reading on winnipegfreepress.com

- Read the E-Edition, our digital replica newspaper

- Access News Break, our award-winning app

- Play interactive puzzles

*No charge for 4 weeks then price increases to the regular rate of $19.00 plus GST every four weeks. Offer available to new and qualified returning subscribers only. Cancel any time.

Monthly Digital Subscription

$4.75/week*

- Enjoy unlimited reading on winnipegfreepress.com

- Read the E-Edition, our digital replica newspaper

- Access News Break, our award-winning app

- Play interactive puzzles

*Billed as $19 plus GST every four weeks. Cancel any time.

To continue reading, please subscribe:

Add Free Press access to your Brandon Sun subscription for only an additional

$1 for the first 4 weeks*

*Your next subscription payment will increase by $1.00 and you will be charged $16.99 plus GST for four weeks. After four weeks, your payment will increase to $23.99 plus GST every four weeks.

Read unlimited articles for free today:

or

Already have an account? Log in here »

Hey there, time traveller!

This article was published 13/04/2022 (1334 days ago), so information in it may no longer be current.

The Bank of Canada’s latest move to combat soaring inflation will have Manitobans paying more on mortgages, loans and lines of credit.

The central bank raised its policy interest rate half a percentage point — its biggest increase in over two decades — to one per cent Wednesday.

Further rate hikes are coming, the Bank of Canada announced.

“Because the rates have been so low for the last two years, this boost… to some extent is getting interest rates back to a longer-term norm or average,” said Fletcher Baragar, an economics professor at the University of Manitoba.

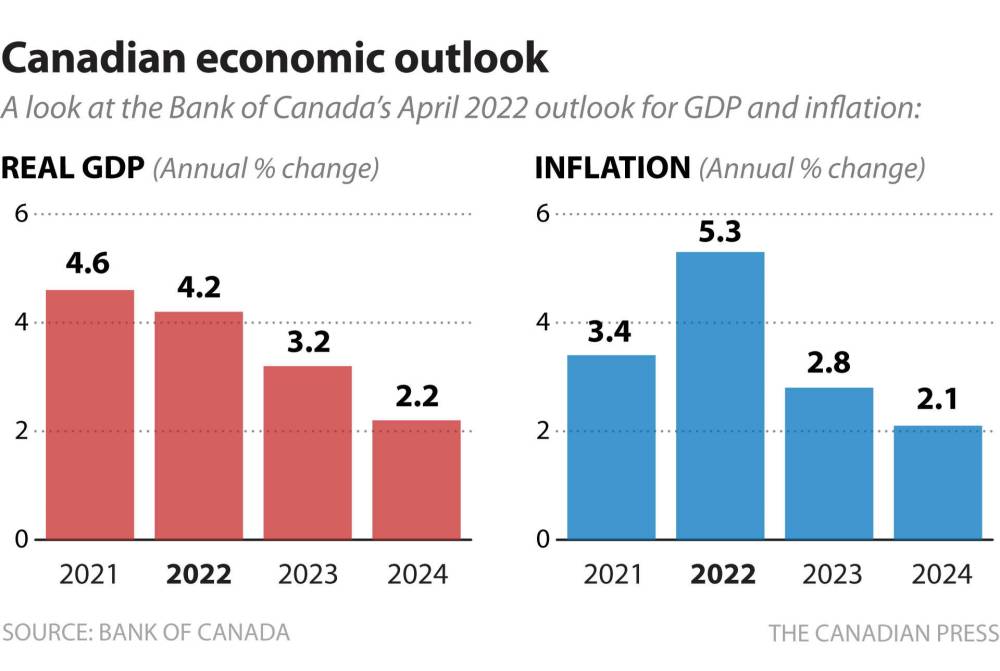

Inflation hit 5.7 per cent nationally in February, surpassing the bank’s expectations. Statistics Canada noted that the inflation rate was the highest it’s been since August 1991.

“The invasion of Ukraine has driven up the prices of energy and other commodities, and the war is further disrupting global supply chains,” said Bank of Canada governor Tiff Macklem. “We are also concerned about the broadening of price pressures in Canada.”

Inflation is expected to stay elevated for longer than the bank initially believed, Macklem said.

So, interest rates will continue to rise at set points throughout the year in an effort to halt rising prices.

“There is some sense of urgency here from the bank,” said Pedro Antunes, The Conference Board of Canada’s chief economist.

Rate increases usually come at a quarter of a percentage point, he noted.

“Because the rates have been so low for the last two years, this boost… to some extent is getting interest rates back to a longer-term norm or average”

– Fletcher Baragar, University of Manitoba economics professor

“(They) reduce, essentially, our disposable income,” he said. “This will take some heat off of housing markets, off of consumer spending.”

The last time the central bank raised its key interest rate by half a percentage point was in May of 2000.

The increase announced Wednesday is expected to prompt Canada’s big banks to raise their prime rates — a change that will increase the cost of loans linked to the benchmark, including variable-rate mortgages.

RBC, TD Bank, CIBC, BMO and Scotiabank all said they’d raise their prime rates by half a percentage point to 3.20 per cent from 2.70 per cent, effective Thursday.

Lately, many Manitoba home sales have ended in bidding wars, with some houses selling for $100,000 over listing price.

“There is no supply,” said Denis Brunet, owner of Mortgage Architects. “People are getting more and more frustrated because they’ve looked at 15 or 20 or 40 houses.”

The interest rate hike won’t solve the supply problem, but it will “take some people out of the market,” Brunet said.

The amount of money needed to enter fixed rate mortgages — deals where, once signed, the regular payment doesn’t change — has increased, meaning more people might look to variable rate mortgages, which are easier to enter but fluctuate as interest rates do.

“Because interest rates have risen so much over the past few weeks, many people will have to get their mortgage pre-approval refreshed or redone to ensure that they’re qualified at the current rates,” said Adrian Schulz, a director with the Manitoba Real Estate Association.

“There is no supply, People are getting more and more frustrated because they’ve looked at 15 or 20 or 40 houses.”

– Denis Brunet, owner of Mortgage Architects

He said variable rate mortgages could be a viable option for homebuyers who no longer qualify for fixed rate mortgages.

Overall housing prices likely won’t decrease, Schulz predicted.

“I think pricing will remain stable and continue to increase just because of the shortage of inventory,” he said.

Most items likely won’t revert to pre-pandemic costs, even with inflation being curbed, Antunes said.

“Within the basket (of purchasable goods), some will come down, some will stay high, but… overall, we don’t actually see the prices coming back down,” he said. “We see the prices staying at elevated levels.”

Oil and food costs could “settle,” he said.

Prof. Baragar said oil prices may decrease a bit, but not much, especially with carbon taxes and a push to more environmentally friendly forms of fuel.

The goal of controlling inflation is to prevent prices from getting — and staying — even higher. The Bank of Canada targets an inflation rate of two to three per cent. A neutral rate neither stimulates nor weighs on the economy, the bank said.

“We think it’ll take until 2024 before inflation is kind of back down to that two per cent range,” Antunes said.

His forecast is echoed by the central bank itself, who expects inflation to ease to two and a half per cent by the second half of 2023 after an average six per cent in the first half of 2022.

The Bank of Canada is also enacting quantitative tightening, as of April 25. It won’t buy bonds from Ottawa, and it will let the bonds it had bought expire.

It purchased billions in government bonds at the start of the pandemic to keep money flowing when the economy halted.

The tightening will affect interest rates in the longer term, Antunes said.

Higher interest rates might dampen demand, but it doesn’t fix issues on the supply side, including disruptions due to the war in Ukraine and the pandemic, Baragar said. So, prices could still increase.

The hiked rate may prevent businesses from undertaking projects to fix supply issues, Baragar said.

“You need business investment, and if you raise the interest rates to try to cool down spending, part of the spending you’re going to cool down is that investment spending that you actually need,” he said. “It’s a tricky sort of situation.”

If inflation continues increasing at a rapid pace, staff may go to their employers and ask for raises, pushing up the cost of goods and services, Antunes noted.

The Bank of Canada’s next interest rate announcement is set for June 1. Its next monetary policy report, which includes an updated outlook on the economy and inflation, is scheduled for release July 13, as is the bank’s interest rate decision.

It slashed the interest rate from 1.75 per cent to a quarter of a percent in 2020 as a response to the COVID-19 pandemic.

– With files from the Canadian Press

gabrielle.piche@winnipegfreepress.com

Gabby is a big fan of people, writing and learning. She graduated from Red River College’s Creative Communications program in the spring of 2020.

Our newsroom depends on a growing audience of readers to power our journalism. If you are not a paid reader, please consider becoming a subscriber.

Our newsroom depends on its audience of readers to power our journalism. Thank you for your support.

.jpg?h=215)