Affordability catch-22 Home prices fall as interest rates continue to rise, increasing inventory while decreasing sales

Read this article for free:

or

Already have an account? Log in here »

To continue reading, please subscribe:

Digital Subscription

One year of digital access for only $75*

- Enjoy unlimited reading on winnipegfreepress.com

- Read the E-Edition, our digital replica newspaper

- Access News Break, our award-winning app

- Play interactive puzzles

*Billed as $5.77 plus GST every four weeks. After 52 weeks, price increases to the regular rate of $19.95 plus GST every four weeks. Offer available to new and qualified returning subscribers only. Cancel any time.

Monthly Digital Subscription

$4.99/week*

- Enjoy unlimited reading on winnipegfreepress.com

- Read the E-Edition, our digital replica newspaper

- Access News Break, our award-winning app

- Play interactive puzzles

*Billed as $19.95 plus GST every four weeks. Cancel any time.

To continue reading, please subscribe:

Add Free Press access to your Brandon Sun subscription for only an additional

$1 for the first 4 weeks*

- Enjoy unlimited reading on winnipegfreepress.com

- Read the E-Edition, our digital replica newspaper

- Access News Break, our award-winning app

- Play interactive puzzles

*Your next Brandon Sun subscription payment will increase by $1.00 and you will be charged $17.95 plus GST for four weeks. After four weeks, your payment will increase to $24.95 plus GST every four weeks.

Read unlimited articles for free today:

or

Already have an account? Log in here »

Hey there, time traveller!

This article was published 14/10/2022 (1378 days ago), so information in it may no longer be current.

A couple of weeks ago, an RBC economics report came out with a headline that read, “Buying a home has never been so unaffordable in Canada.”

While that may be the case for many first-time buyers, for Hashm Abdulla, 24 — who, along with his partner Sydney Froese, just bought their first home last month in the Lord Roberts neighbourhood — the alternative was just as bad.

“Regardless of interest rates, it was more economical for us to buy than to stay renting,” Abdulla said. “Sure, we’re worried about interest rates, but rent can go up too. Rents were going up. At least now, at some point all that money will come back to us.”

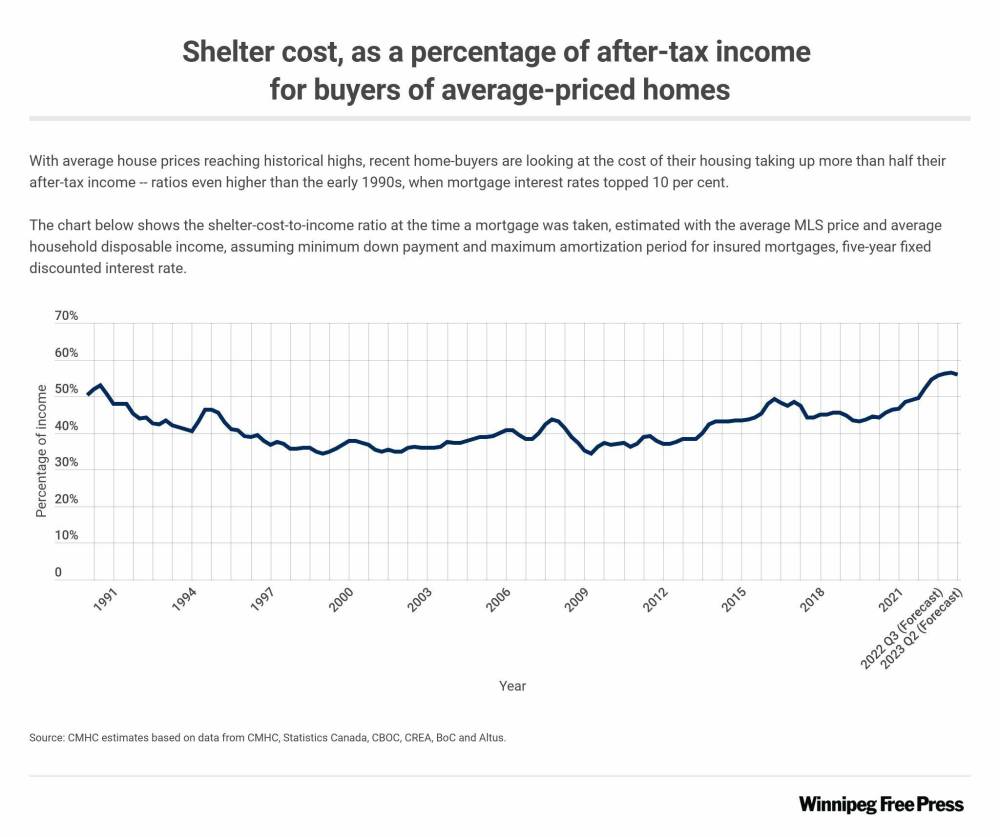

A Canada Mortgage and Housing Corp. report released Thursday concurred with the RBC report showing that affordability has not been this low since 1990, when interest rates were at 10 per cent. (They’re at five to six per cent now.)

The report forecasts housing prices will continue to drop into 2023 but, Patrick Perrier, CMHC’s deputy chief economist, said it won’t help affordability much because the lower prices will be offset by higher interest rates and an increasingly competitive rental market.

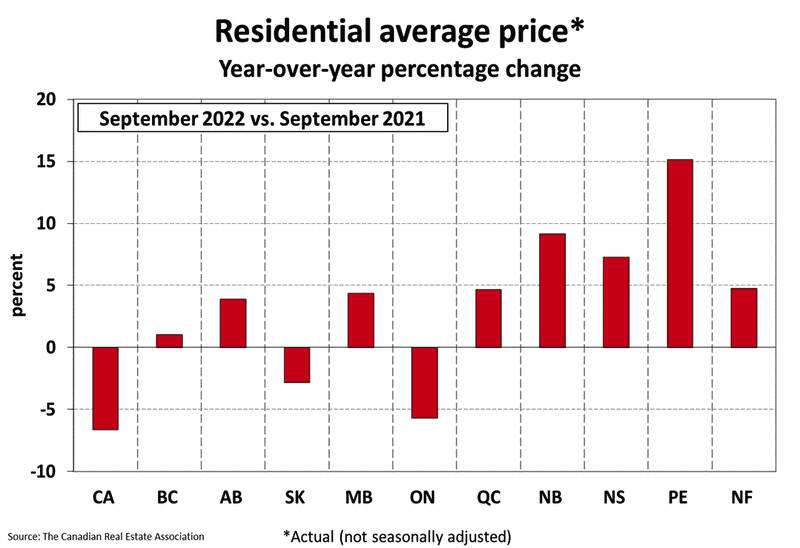

CMHC’s home price forecasts were mirrored by the Royal LePage House Price Survey, also released this week, which showed that while average Winnipeg home prices increased by 6.1 per cent in the third quarter compared to the same time last year, they also declined by 5.1 per cent compared to the second quarter of this year.

Perrier expects the national average home price to fall 15 per cent from $770,812 — the peak seen in the first quarter of this year — by the end of the second quarter of 2023.

While the year-over-year increase and quarter-to-quarter decrease in Winnipeg prices were significant, they are nowhere near the double-digit year-to-year price increases in some places and quarter-over-quarter declines were close to 10 per cent in the Greater Toronto Area.

Michael Froese, broker and manager at Royal LePage Prime Real Estate in Winnipeg, said the 18-month pandemic housing boom caused by pent-up demand, low interest rates, cheap cash and low inventory was a perfect storm for prices to escalate the way they did.

“Everything was selling; it did not really matter the condition of the house,” he said. “Now the homes that are well-positioned in the market, well-staged, well-taken-care-of are the ones that see the most attention.”

Froese said that while the Winnipeg market may be cooling a little, it is still more calm than many other parts of the country. The relative level of concern is dependent on the lens through which one considers the situation.

“How far do you want to turn back the clock?” Froese said. “If you take away the last two years, in 2019 interest rates were rising, there was a similar sales-to-listing relationship… we’re very close to 2019 now and in 2019 we were all happy.”

Inventory levels in Winnipeg are creeping back to pre-pandemic levels, but there will still be about 1,000 fewer in 2022 than were on the market in 2019.

“Now that demand has dipped and supply is increasing, it means prices will go down, which they are,” he said.

As are sales. On Friday, the Canadian Real Estate Association reported that September sales across the country were down 32.2 per cent compared to September 2021

Jill Oudil, chair of CREA, said “It makes for an interesting dynamic, one that doesn’t really have many historical precedents. The market has changed so much in the last year, and the adjustment to higher borrowing costs is still underway.”

Froese and Akash Bedi, broker and owner of RE/MAX Executives Realty in Winnipeg, both suggest that despite the higher interest rates and the larger mortgage payments that come with it, the current market conditions could actually make it a good time for first-time buyers to enter the market.

“If they were priced out of the market earlier in the year, even up to June, because of the market conditions where there were multiple offers on many homes, now they can come and they may have the chance to negotiatea favorable price,” Bedi said.

But Robert Hogue, assistant chief economist at RBC, said, while the RBC’s analysis of housing affordability is greatly influenced by the red hot housing markets of Ontario and British Columbia, Manitoba is not immune.

“The deterioration in affordability over the past year is a broad trend across Canada, including Winnipeg,” he said.

As to whether or not the softening in demand and prices provide first-time buyers with a bit of space to enter the market, he’s not so sure.

“Mortgage rates have gone up considerably so at the end of the day those ownership costs — the biggest chunk of it is your mortgage payments — are still up relative to what it was a year ago or three months ago, even though prices have started to decline,” he said.

CMHC’s Perrier, who has joined a growing list of economists who now say the country will slip into a mild recession likely by the end of the year and start recovering by the third quarter of next year, said that when housing is so unaffordable it puts a huge damper on demand across the economy.

“Rates are rising not just for households but for business as well,” Perrier said in an interview with the Free Press. “That contributes to an economic slowdown. It also has an impact on labour market and slows income growth.”

The only glimmer of optimism in Perrier’s report is that national housing starts are picking up and are currently well out-pacing pre-pandemic averages.

“But it is still not sufficient,” he said. “We need to double the pace of housing starts if we want to achieve affordability by 2030, which is very ambitious, but it is a good step forward.”

martin.cash@freepress.mb.ca