As Canada faces potential recession, Freeland to give fall economic statement Nov. 3

Advertisement

Read this article for free:

or

Already have an account? Log in here »

To continue reading, please subscribe:

Digital Subscription

One year of digital access for only $75*

- Enjoy unlimited reading on winnipegfreepress.com

- Read the E-Edition, our digital replica newspaper

- Access News Break, our award-winning app

- Play interactive puzzles

*Billed as $5.77 plus GST every four weeks. After 52 weeks, price increases to the regular rate of $19.95 plus GST every four weeks. Offer available to new and qualified returning subscribers only. Cancel any time.

Monthly Digital Subscription

$4.99/week*

- Enjoy unlimited reading on winnipegfreepress.com

- Read the E-Edition, our digital replica newspaper

- Access News Break, our award-winning app

- Play interactive puzzles

*Billed as $19.95 plus GST every four weeks. Cancel any time.

To continue reading, please subscribe:

Add Free Press access to your Brandon Sun subscription for only an additional

$1 for the first 4 weeks*

- Enjoy unlimited reading on winnipegfreepress.com

- Read the E-Edition, our digital replica newspaper

- Access News Break, our award-winning app

- Play interactive puzzles

*Your next Brandon Sun subscription payment will increase by $1.00 and you will be charged $17.95 plus GST for four weeks. After four weeks, your payment will increase to $24.95 plus GST every four weeks.

Read unlimited articles for free today:

or

Already have an account? Log in here »

Hey there, time traveller!

This article was published 28/10/2022 (1382 days ago), so information in it may no longer be current.

OTTAWA – A looming recession and Canada’s need to keep up with the United States on clean energy investments will be front and centre next week when Finance Minister Chrystia Freeland delivers her fall mini-budget.

Freeland has already warned not to expect big money to help Canadians cope with lingering inflation, stressing in recent weeks that would just further fuel inflation.

“We can’t support every single Canadian in the way we did with the emergency measures that we put in place at the height of the pandemic,” she said Oct. 19 in a speech to the Automotive Parts Manufacturers’ Association in Windsor, Ont.

But she signalled that Canadians can expect a fall economic statement that focuses on the economy Canada is trying to “seize” for the future — namely one that is heavily focused on clean power, electric vehicles, battery manufacturing and critical minerals.

She has said the statement will include the first part of Canada’s response to the United States Inflation Reduction Act, which included nearly $400 billion for green energy and climate change.

Natural Resources Minister Jonathan Wilkinson shed more light on what that might look like in a speech in Toronto on Wednesday. The legislation’s tax incentives for hydrogen power production, critical minerals and battery manufacturing are among Canada’s biggest concerns, he said.

“There are a few areas like that, where, you know, I think Minister Freeland has been clear, and I’ve been clear that I think we will need to respond,” he said.

“I’m not going to tell you when we’re going to respond, but we will need to respond. Because at the end of the day, we want to ensure that there is a competitive place for folks to make investments in Canada.”

On top of competing for investments, there are concerns that there are only so many skilled workers and supplies to get the projects going and that Canada will find itself at the back of line if its investments don’t keep pace.

Wilkinson also said in a discussion at a net-zero conference in Ottawa earlier this month that he was talking with Freeland about making investments in clean power to both meet Canada’s growing electricity needs and ensure 100 per cent of that electricity comes from non-emitting or renewable sources.

Canada’s 2022 budget included a tax credit of 30 per cent for clean hydrogen production and about 50 per cent for carbon capture and storage. The latter is technology that traps carbon dioxide emissions at their source — mainly big industrial plants and electricity generating stations — and funnels them back underground.

Carbon capture is the main way Canadian oil and gas producers will meet their emissions targets and regulations, though environment groups warn the technology is still unproven on large scales.

But the U.S. Inflation Reduction Act came in with much more generous tax incentives for hydrogen and carbon capture, and Freeland is looking at how to close that gap. If it doesn’t happen in the fiscal update coming Nov. 3, the next budget will likely include such measures.

Though inflation is slowing — down to 6.9 per cent in September compared with a high of 8.1 per cent in June — it remains one of the biggest concerns both for Canadians and the government.

Randall Bartlett, senior director of Canadian economics at Desjardins, said he expects the government to stick to its commitment on fiscal discipline given the current economic climate.

“I don’t think the federal government wants to work to fight against the Bank of Canada by putting in measures that will increase inflation,” Bartlett said.

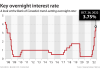

The Bank of Canada has been combating decades-high inflation with aggressive interest rate hikes since March. The central bank raised interest rates this week for the sixth time this year, with the half-percentage point rate hike bringing its key interest rate to 3.75 per cent.

Both the bank and Freeland have warned of an economic slowdown, and possibly a recession.

Robert Asselin, senior vice-president with the Business Council of Canada, says fiscal discipline is especially important as the country faces high inflation, rising interest rates and low economic growth.

“The focus now should be on fiscal prudence to ensure the central bank can bring inflation back to its mandated target range,” Asselin said in a statement.

Desjardins forecasts the federal deficit to come in around $20 billion at the end of the fiscal year, though Bartlett notes that doesn’t include any spending that could be announced in the fall economic statement.

Monthly updates from the Finance Department have shown that federal finances have been improving as revenues have risen and COVID-19 pandemic spending has wound down.

In the first five months of the 2022-23 fiscal year, the federal government posted a $3.9 billion surplus compared to a deficit of $57.2 billion reported for the same period last year.

Bartlett says federal finances have been improving more than anticipated because of Canada’s tight labour market pushing up wages, corporations raking in high profits and inflation boosting tax revenues.

This report by The Canadian Press was first published Oct. 28, 2022.

Related Articles

Canadian economy grew 0.1% in August, continuing on path of modest growth

Advertisement Advertise With Us

Advertisement Advertise With Us